Mistakes Travelers Make with Currency Converters

Avoid common currency conversion errors—DCC traps, ATM and exchange fees, over-converting cash, and local pricing tips to keep more of your travel budget.

If you’re traveling abroad, currency conversion mistakes can quietly drain your budget. From hidden fees to poor exchange rates, these errors can add hundreds of dollars to your trip. Here’s what you need to know to avoid the most common pitfalls:

- Airport Exchanges Are Costly: Avoid airport kiosks like those at DFW or Dallas Love Field - they often have rates 3–5% worse than the market.

- Dynamic Currency Conversion (DCC) Adds Extra Fees: Always pay in the local currency instead of USD to avoid a 7–10% markup.

- Hidden Fees Add Up: ATM charges, foreign transaction fees, and exchange counter markups can quickly become expensive.

- Converting Too Much Cash: Exchanging large amounts upfront can leave you with leftover currency that’s costly to convert back.

- Ignoring Local Currency Practices: Paying in USD at tourist spots or misjudging local prices can cost more than you realize.

Key Tip: Use bank-affiliated ATMs, credit cards with no foreign transaction fees, and reliable mid-market rate sources to minimize costs. Plan ahead to keep more of your money for the experiences that matter.

Currency Conversion Costs Comparison: How Fees Add Up When Traveling

10 Travel MONEY MISTAKES Everyone Makes & How to Avoid Them! 💸💰😳 Essential Hacks and Travel Tips ✈️🌎

Mistake 1: Misreading Currency Converter Rates

When you check a currency converter app and see that 1 USD equals 0.90 EUR, it’s easy to assume that’s the exact rate you’ll get when making purchases or withdrawing cash. But that number represents the mid-market rate - the rate banks use when trading currencies with each other, without any added fees. Unfortunately, it’s not the same as the retail rate, which includes markups and transaction fees.

The Difference Between Mid-Market and Retail Rates

The retail rate adds a margin - usually a few percentage points above the mid-market rate - along with fees from banks, credit card companies, or exchange services.

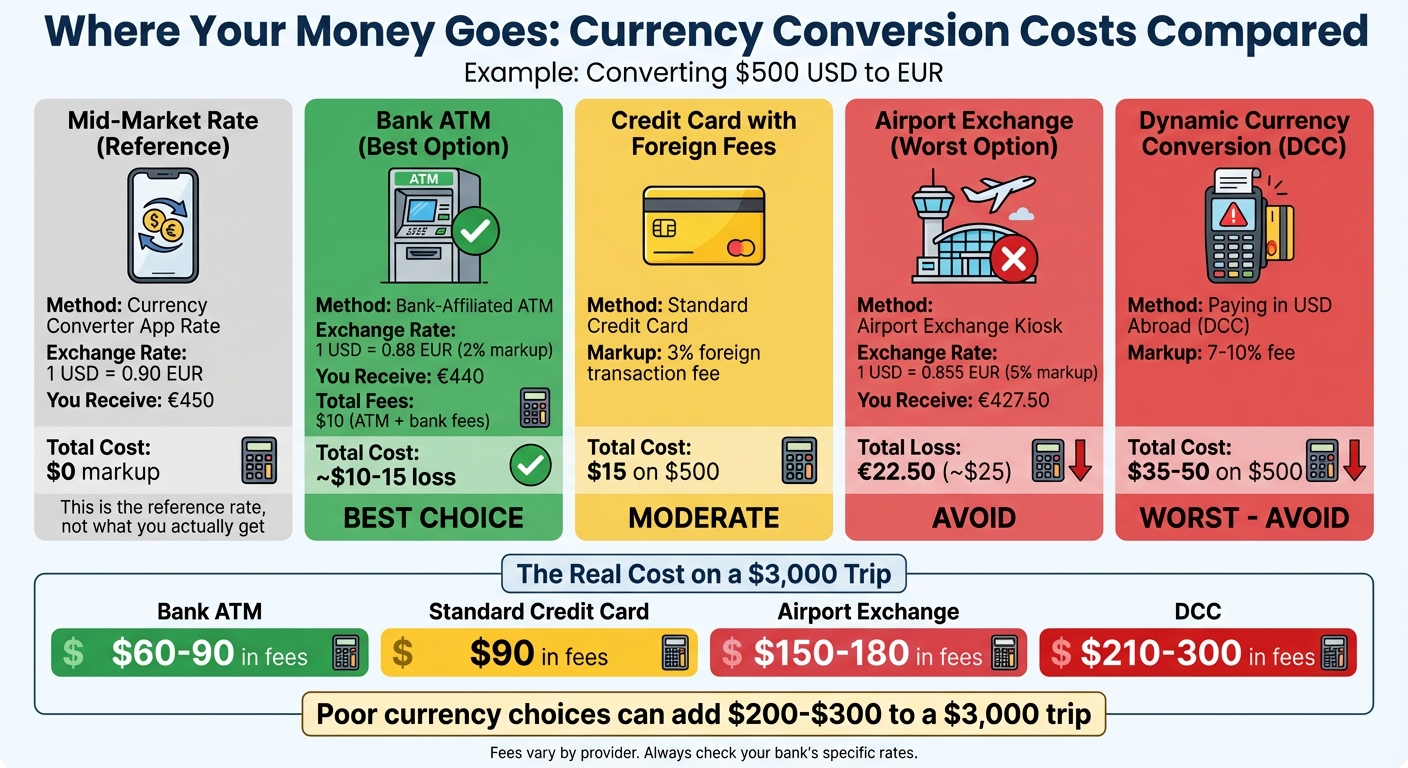

For instance, if the converter shows 1 USD = 0.90 EUR, you might think $500 will get you €450. But at an airport exchange counter with a 5% markup, you might receive a rate closer to 1 USD = 0.855 EUR. That means your $500 would convert to roughly €427.50 - over €20 less than expected. On a $2,000 trip to Europe, a spread of 3–6% could add $60–$120 in extra costs. If exchange rates change during your trip, this difference can grow even larger.

Overlooking Rate Fluctuations

Exchange rates don’t stay static - they shift constantly due to factors like economic reports, interest rate changes, and geopolitical events. Checking rates once before your trip isn’t enough. For example, if you plan your budget around an exchange rate of 1 USD = 0.95 EUR but the rate drops to 0.90 EUR, every $1,000 you spend in Europe could cost you about $56 more. Over the course of a vacation, these small changes can add up to hundreds of dollars.

Even if you score a great deal on airfare with Joe's Flights from DFW or Love Field, unexpected currency shifts can eat into your savings. Keeping an eye on exchange rates throughout your trip can help you avoid these surprises and make better financial decisions.

Tips to Avoid Currency Conversion Mistakes

Before traveling, review your bank or credit card’s foreign transaction fees and currency conversion policies, which are usually detailed in your cardholder agreement. Some banks partner with international networks to reduce ATM fees or offer cards with zero foreign transaction fees - both of which can save you money.

When planning your budget, factor in an extra 3–5% for cards with low fees and 5–8% for standard cards or airport exchanges. For example, if a restaurant bill in Europe is $80 at the mid-market rate, budgeting $84–$86 gives you some breathing room for added fees. Being realistic about these costs can help you stick to your travel budget.

Once you’re on your trip, check current exchange rates regularly using a reliable mid-market rate source, especially for common currency pairs like USD/EUR or USD/MXN. Review your recent card transactions to understand the effective rate you’re being charged. To avoid locking in a bad rate, consider withdrawing smaller amounts of cash more frequently instead of taking out a large sum all at once. This approach can help reduce the impact of unfavorable rate changes.

Mistake 2: Forgetting About Hidden Fees

Currency converters may show you the base exchange rate, but they often leave out the hidden fees that can creep in. For instance, withdrawing $200 from an ATM overseas might cost much more than you expect once all the fees are added.

ATM and Foreign Transaction Fees

Using ATMs abroad can come with a mix of charges. These typically include an operator surcharge that ranges from $5 to $10, a bank fee of $2 to $5, and a 3% foreign transaction fee.

Let’s break it down: if you withdraw $200, you might face a $5 ATM surcharge, an additional $5 in bank fees, and around $6 in foreign transaction fees. That’s $16 in extra costs just to access your money. And if you’re using ATMs at airports or hotels, the fees and exchange rates are often even worse, giving you less value for your cash.

Exchange Counter Markups

Airport exchange counters might lure you in with "no commission" promises, but their exchange rates can be 3–5% worse than the mid-market rate. Here’s what that means: if you exchange $500 at an airport kiosk with a 5% markup, you’re effectively losing $25 right off the bat. These hidden costs can add up fast, so being aware of them is crucial.

How to Reduce Fee Costs

To minimize these fees, start by checking with your bank or reviewing your credit card’s terms to understand the charges for foreign transactions and ATM withdrawals. Some banks have agreements with international networks that waive ATM fees, and certain travel rewards credit cards don’t charge foreign transaction fees.

When withdrawing cash abroad, stick to ATMs operated by major international banks like HSBC, Barclays, or Santander. Avoid unbranded machines in tourist-heavy areas, as they tend to come with higher fees. Also, when the ATM offers to let you pay in USD instead of the local currency (a practice called Dynamic Currency Conversion), always decline. According to Clark Howard, opting to pay in USD can cost you an extra 7–10% per transaction.

To stay ahead, calculate the total cost of exchanging money by factoring in your bank’s fees - like the 3% foreign transaction fee and any ATM surcharges. Knowing the real cost per dollar exchanged can save you from unpleasant surprises when you check your bank statement later.

Mistake 3: Accepting Dynamic Currency Conversion (DCC)

Dynamic Currency Conversion (DCC) might seem convenient, but it often comes with a hefty price tag - adding an extra 7–10% to each transaction.

Why DCC Is More Expensive

With DCC, the conversion rate is set by the operator, not the market, and typically includes a markup of 5–10% on top of the mid-market rate. For example, if the mid-market rate is 1.10 USD/EUR, DCC providers might offer a rate that's 8–10% higher.

DCC is often marketed as a "helpful service", but in reality, it hides inflated fees. Many terminals are programmed to display your home currency by default, making it easy to unknowingly accept the pricier rate.

Let’s explore where you’re most likely to encounter this.

Common Places You’ll See DCC

- ATMs: You might see prompts like "Display in USD?"

- Point-of-sale terminals: These often ask if you want to pay in USD.

- Hotels and booking websites: At tourist hotspots, hotel front desks or online booking platforms may offer to charge you in USD instead of the local currency.

For instance, imagine a €50 restaurant bill in Paris. With DCC, the terminal might show an option to pay "$57.50 USD", but if you decline and let your card network handle the conversion, you’d only pay $55.00 USD.

How to Avoid DCC Fees

The solution is straightforward: always choose to be charged in the local currency. If an ATM asks, "Would you like to see this amount in USD?", select "No" or "Continue in local currency." Similarly, at payment terminals, opt for the local currency whenever prompted.

If the terminal doesn’t give you a choice and only shows the local currency, you’re safe - DCC isn’t being applied. To double-check, review your statement to ensure the conversion falls within a 1–3% range. Anything higher likely means DCC was used.

sbb-itb-d0f92e0

Mistake 4: Converting the Wrong Amount of Money

After tackling the challenges of rates and fees, another frequent misstep travelers make is converting an incorrect amount of money.

Many people use a currency converter to estimate their trip budget in local currency, then exchange the entire amount in cash before or right after arriving. This approach often leaves them with leftover currency that either has to be reconverted at a loss or, worse, includes coins that can’t be exchanged at all.

Converting Too Much Cash at Once

Exchanging a large sum based on a single app’s rate may seem convenient, but it locks you into that rate for the entire trip. This doesn’t account for your actual spending habits or the way payments are typically handled in your destination. Exchange providers often see travelers converting large amounts “just in case,” only to face poor rates when trying to exchange leftover bills. If you’re converting your entire budget at airports or hotels - which typically offer the worst rates - you’re likely paying a premium twice: once to buy the foreign currency and again when converting unused funds back to dollars.

Beyond the financial downside, carrying a lot of cash increases the risk of theft and the hassle of keeping it secure during your trip. Travel expert Rick Steves points out that coins are almost never exchangeable, so leaving a country with a pocketful of coins is essentially wasting money.

Relying Only on Cash or Only on Cards

In some destinations, like parts of the U.K., New Zealand, or South Korea, cashless payments are the norm. Relying solely on cash in these places can be inconvenient for things like public transit, attractions, or many shops. On the other hand, in cash-heavy countries such as Egypt, Morocco, or the Philippines, cards may not be widely accepted for taxis, small eateries, or markets. Travelers who assume they can "tap everywhere" might find themselves in a bind late at night, scrambling for cash and forced to use out-of-network ATMs with high fees and poor exchange rates.

A balanced approach can help you avoid these pitfalls.

How to Convert Smarter

The best strategy? A hybrid approach. Carry a small amount of local cash for everyday purchases like transit fares, tips, and market finds, while using a no-foreign-transaction-fee credit or debit card for larger expenses like hotels and dining. Stick to bank-affiliated ATMs to withdraw just enough cash for a few days, and top up as necessary.

Before you leave, research whether your destination leans more cashless, mixed, or cash-heavy. Look into whether public transit supports contactless payments and if small businesses accept major U.S. card networks. Toward the end of your trip, scale back ATM withdrawals and shift more purchases onto your cards. If you have leftover bills, use them for airport meals or duty-free shopping before boarding - it’s usually a better option than converting small amounts back into U.S. dollars.

Mistake 5: Ignoring Local Currency Customs

Even if you've got exchange rates, fees, and dynamic currency conversion figured out, there's another layer that often trips up U.S. travelers: local pricing habits. While your converter app might show that 100 euros equals $109, it doesn't account for the quirks of local pricing or how businesses handle currency.

Paying in USD at Unfavorable Exchange Rates

In popular tourist spots, you'll frequently see signs at shops, hotels, or even street vendors saying they "accept U.S. dollars." At first glance, it seems convenient, but here's the catch: these businesses usually apply their own exchange rates, which are almost always skewed in their favor. Consumer advocate Clark Howard warns that paying in dollars instead of the local currency can quietly add 7–10% to your total cost compared to paying in local currency and letting Visa or Mastercard handle the conversion at their wholesale rate. That’s an extra fee you might not even notice.

This sneaky practice is common at hotel check-ins where the payment terminals default to USD, car rental counters with pre-converted payment slips, or with taxi drivers and market vendors who quote prices in rounded-off dollars. The solution? Always insist on pricing and paying in the local currency. If you're at a payment terminal, choose the local currency option when prompted. If a merchant quotes you in dollars, ask for the price in their currency and compare it to your converter's mid-market rate to see if the rate is fair.

Misjudging Local Price Levels

Your currency converter might tell you that 50 pesos equals $2.75, but it won’t tell you if that’s a typical price for a cup of coffee in Mexico City or if you’re being overcharged. Without understanding the local cost of living, it’s easy to miscalculate your budget. What feels like a bargain in one country might actually be overpriced in another due to factors like local wages, tourist markups, or neighborhood-specific pricing.

Before your trip, research average daily budgets for your destination using reliable travel guides or traveler forums. Look up the typical costs for activities you’re planning - like dining at a restaurant, booking tours, or using rideshares. This will help you create a realistic budget instead of relying on a general rule like "$100 per day." Knowing local price norms will make it easier to identify when you're getting a fair deal.

How to Adapt to Local Pricing Practices

Blend your converter’s math with on-the-ground knowledge. Find out if your destination relies more on cash or cards, whether tipping is customary or included in bills, and if haggling is the norm in markets. During your first day, ask hotel staff about typical prices for common purchases to help you gauge costs. Memorize a few quick conversions (like "10 local units ≈ $3") to make price comparisons easier.

For Dallas travelers using Joe's Flights, consider reallocating some of the money you saved on airfare to cover potential currency inefficiencies. This buffer can help you handle unexpected expenses, higher-than-expected local prices, or a few rookie mistakes. After a couple of days abroad, compare your actual spending to your initial estimates, and adjust your budget or activities as needed. By combining converter rates with local insights, you’ll turn your currency converter into a tool for smarter, more informed travel planning.

Conclusion

Flying out of DFW or Love Field? Scoring a great flight deal is only part of the equation. Poor currency conversion choices can quietly drain your budget - potentially adding $200–$300 to a $3,000 trip. That’s money you could’ve spent on an extra night’s stay, a memorable meal, or a unique local experience.

The good news? A few simple steps can keep more cash in your pocket. Always opt for local currency when paying abroad, stick to bank ATMs for cash withdrawals, use credit cards with no foreign transaction fees, and only withdraw cash when absolutely necessary. Before you leave Dallas, take a moment to review your cards’ international fees, check the mid-market exchange rate for your destination, and plan how much you’ll rely on cash versus cards based on where you’re headed.

If Joe's Flights helps you snag a $550 roundtrip to Europe instead of $900, pairing those savings with smart currency practices could stretch your travel budget even further. By managing your money wisely, you’re not just saving - you’re creating more room for unforgettable travel experiences.

FAQs

What’s the best way to avoid hidden fees when using currency converters while traveling?

When using currency converters, it's important to watch out for hidden fees. Always verify whether the total amount includes transaction fees or exchange rate markups. Opt for reliable services that clearly show the full amount in USD and use current exchange rates.

Be cautious of converters offering rates that seem unusually low - they often come with hidden charges. To ensure you're not overpaying, compare the converter's rate with those offered by your bank or credit card provider. This simple step can help you avoid unnecessary costs.

What is Dynamic Currency Conversion, and why is it better to avoid it?

Dynamic Currency Conversion (DCC) is a service that allows you to pay in your home currency when using your credit or debit card overseas. While it might sound like a handy option, it typically comes with steeper exchange rates and additional fees, which can make your purchase pricier than if you had chosen the local currency.

To avoid unnecessary costs and secure a better exchange rate, it's smarter to pay in the local currency whenever you're given the choice. This ensures that your bank or card issuer processes the conversion, which is usually more cost-effective.

Why should travelers use bank-affiliated ATMs for foreign currency withdrawals?

When you need to withdraw foreign currency, bank-affiliated ATMs are usually your best bet. They often come with lower fees and more favorable exchange rates compared to non-bank or airport ATMs, which tend to charge higher fees and offer less advantageous rates. These extra costs can pile up quickly during your travels.

To cut down on expenses, stick to ATMs linked to well-known banks. Additionally, consider withdrawing larger sums in one go to reduce the impact of transaction fees.

Related Blog Posts

Written by Joe's Flights. Spotted something cheaper? Tell us.