10 Ways to Save for Travel Emergencies Fast

Small, consistent savings and simple swaps build a travel emergency fund fast — automate transfers, cut extras, use round-ups and keep funds separate.

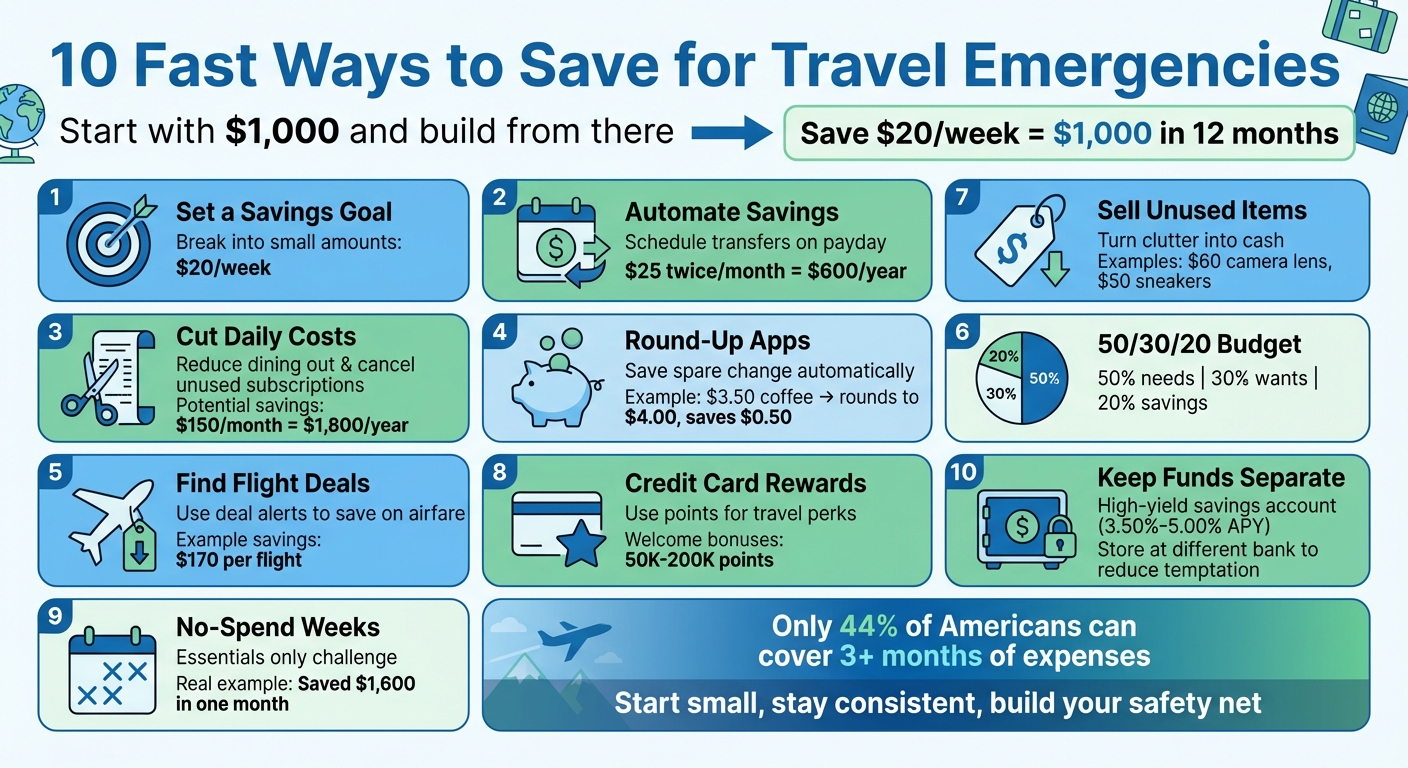

Need a quick financial cushion for unexpected travel expenses? Here are 10 actionable ways to save for emergencies like sudden medical bills, flight changes, or repairs. Start small with a $1,000 target and build from there. Here's how:

- Set a Savings Goal: Break it into smaller, manageable amounts - like $20 per week.

- Automate Savings: Schedule transfers or split your paycheck to save effortlessly.

- Cut Daily Costs: Reduce dining out, cancel unused subscriptions, and track expenses.

- Use Round-Up Apps: Save spare change from every purchase.

- Find Flight Deals: Use services like Joe's Flights to save on airfare.

- Follow a Budget: The 50/30/20 rule helps balance needs, wants, and savings.

- Sell Unused Items: Turn clutter into cash through platforms like OfferUp or Mercari.

- Leverage Credit Card Rewards: Use points for travel perks, but pay balances in full.

- Try No-Spend Weeks: Focus on essentials and save the rest.

- Keep Funds Separate: Use a high-yield savings account to protect your emergency stash.

Key takeaway: Small, consistent actions - like saving $10–$20 weekly - can help you build a reliable travel emergency fund without stress.

10 Fast Ways to Build Your Travel Emergency Fund

Why an Emergency Fund is Important | Debt Free Disney

1. Set a Clear Savings Target

Trying to save three to six months' worth of expenses all at once can feel like climbing a mountain without a trail. Instead, start small and set an achievable goal. Kimberly Palmer from NerdWallet suggests aiming for an initial target of $500. It’s a manageable first step that helps you build momentum without the stress of tackling an entire emergency fund right away.

Once you’ve chosen your target, break it down into smaller, regular contributions. Let’s say your goal is $1,000 in a year. That works out to about $84 per month, $38 per biweekly paycheck, or just $19 per week. Breaking it into bite-sized pieces makes the process feel much more doable.

| Savings Goal | Weekly Contribution | Monthly Contribution | Time to Reach Goal |

|---|---|---|---|

| $500 | ~$10 | ~$42 | 12 Months |

| $1,000 | ~$20 | ~$84 | 12 Months |

| $3,000 | ~$58 | $250 | 12 Months |

To make sure you don’t dip into your savings for non-emergencies, stash your funds in a high-yield savings account. This not only keeps the money separate but also helps it grow over time. Once you hit your first milestone, you can raise your target, building both your savings habit and confidence as you go.

2. Automate Your Savings Transfers

Sticking to a savings plan can be tough, but automating the process makes it much easier. By setting up automatic transfers, you eliminate the need for constant decision-making or relying on willpower. Once it's in place, your money moves directly into your travel emergency fund without you lifting a finger.

There are two easy ways to automate your savings: recurring bank transfers or direct deposit splitting. With recurring transfers, you set a fixed amount or percentage to move from your checking account into your savings account on a regular schedule. Direct deposit splitting, on the other hand, allows you to allocate a portion of your paycheck to go straight into your savings account before it even hits your checking account.

"Inertia and inherent laziness tend to work in our favor. That is, once enrolled in an automatic savings plan, people tend to stay enrolled." - Robert R. Johnson, PhD, CFA, and Professor of Finance, Heider College of Business at Creighton University

Timing your transfers to line up with payday is a smart move. This "pay yourself first" strategy ensures your savings are secured before you have a chance to spend the money elsewhere. Even small, consistent contributions make a difference. For instance, setting aside just $25 twice a month adds up to $600 in a year. If money is tight, start small - saving as little as $5 a week can still lead to noticeable growth over time.

Here’s a helpful tip: rename your savings account to something like "Travel Emergency Fund." This small change can help you resist the temptation to dip into it for non-emergencies. Additionally, setting up balance alerts on your checking account can protect you from overdraft fees when your automated transfers are processed.

3. Cut Unnecessary Daily Spending

Everyday expenses can quietly drain your wallet, but they also offer a chance to grow your travel emergency fund. Start by tracking your expenses for 30 to 60 days to uncover where your money is going. Once you have a clear picture, focus on the areas where spending is highest.

"It's not about cutting coffee - it's about clarity." - Citizens Bank

Some of the biggest culprits include restaurant meals, takeout, and delivery services. Cutting back on dining out and cooking at home instead can save a significant chunk of change. Also, take a close look at your recurring subscriptions - 42% of consumers pay for streaming services they don't even use. Cancel anything you're not actively using, whether it's a gym membership, a magazine subscription, or a premium app you downloaded on a whim.

Impulse purchases can also derail your savings efforts. Try the 24-hour rule: wait a full day before buying anything nonessential. This pause gives you time to decide if the item is a genuine need or just a passing desire. Sometimes, even adding something to your online cart can satisfy the urge without actually spending money.

The key is to channel these savings directly into your travel emergency fund. For example, if you’re spending $150 a month on takeout and unused subscriptions, redirecting that money could add up to $1,800 in a year. That’s a solid financial cushion for unexpected travel expenses.

4. Use Round-Up Savings Apps

If you're already automating transfers and cutting back on spending, round-up savings apps can be a great way to further build your emergency fund - effortlessly.

These apps work like a digital version of a spare change jar. Every time you make a purchase with your debit or credit card, the app rounds up the total to the nearest dollar and transfers the difference into your savings account. For example, if you spend $3.50 on coffee, the app will round it up to $4.00 and deposit the extra $0.50 into your savings. Over time, these small amounts can really add up.

For the best results, link your round-up app to a high-yield savings account. Right now, these accounts are offering competitive annual percentage yields (APYs), which can help your savings grow even faster.

"Some people like to use round-up apps or the 'change jar' method to also boost their savings." – SoFi

The good news? Many banks now offer round-up features directly in their mobile apps - completely free. For example, Bank of America's mobile app includes a Spending & Budgeting tool with built-in round-up functionality. If you're considering opening a new account specifically for this purpose, look for one with no monthly fees and low minimum deposit requirements. Some banks even let you get started with as little as $1.

When combined with automated transfers, round-up savings apps make it easy to grow your fund without even thinking about it.

5. Subscribe to Joe's Flights for Free Deal Alerts

Cutting down on airfare is a smart way to grow your travel emergency fund. Since flights often make up a big chunk of travel expenses, finding cheaper tickets means you can put the extra cash toward your emergency savings. The earlier you start saving on travel costs, the more you'll have set aside for unexpected situations.

In addition to trimming daily expenses or setting up automated savings, snagging flight deals is another way to stretch your budget. Services like Joe's Flights make this easy by sending free alerts for discounted flights from Dallas airports (DFW and Love Field). These notifications help you take advantage of fare drops, so you can save money and boost your emergency fund at the same time.

For example, if you save $170 on a flight by using Joe's Flights, you can take that savings and deposit it directly into your emergency fund.

"Having an emergency fund could be the best travel insurance of all." – CIT Bank

Joe's Flights offers a free plan that sends one deal per week, or you can upgrade to the Premium plan for $59/year to get unlimited alerts. Pairing this approach with other budgeting strategies can help you build a solid travel fund while still enjoying great deals on flights.

6. Follow the 50/30/20 Budget Method

If you're looking for a simple way to manage your money and grow your travel emergency fund, the 50/30/20 method is worth considering. This budgeting framework divides your income into three clear categories: 50% for needs (think rent, groceries, utilities, and insurance), 30% for wants (like dining out, entertainment, or streaming services), and 20% for savings and debt repayment. It’s a practical way to balance your financial priorities while giving savings the attention it deserves.

To grow your emergency fund faster, consider trimming your discretionary spending. For instance, if your monthly income is $3,000, cutting back on wants by just 10% frees up an extra $300 each month. Redirecting that amount to your emergency savings could add up to $3,600 in a year - money that could be crucial during unexpected travel situations.

Take a close look at your recent spending habits. By reviewing a few months' worth of expenses, you can identify areas where you’re overspending and redirect those funds into savings. Once you've set your budget, automate the process by scheduling regular transfers to a high-yield savings account. This way, your money can grow with the help of competitive interest rates. If saving 20% of your income feels overwhelming, start small - $50 to $100 per month can still make a difference. Even at this pace, you could build a $600 to $1,200 safety net in just a year.

The beauty of the 50/30/20 method is its flexibility. If you live in a high-cost area, you can tweak the percentages to fit your situation without losing sight of your savings goal. The most important thing is consistency. As your income increases or your expenses decrease, you can gradually boost your savings rate to reach your travel fund target even faster.

This strategy works well alongside other financial tips, helping you build a reliable safety net for your adventures.

sbb-itb-d0f92e0

7. Sell Items You Don't Use

Got items lying around that you no longer need? Turning them into cash can be a smart way to grow your travel emergency fund. Use resale platforms to sell these items and deposit every dollar you make directly into your fund. This approach works hand-in-hand with automated transfers and spending adjustments, giving your savings a welcome boost.

OfferUp is a great choice for selling larger, local items like furniture, sports gear, or home goods. It connects buyers and sellers in cities like New York, Los Angeles, Chicago, and Houston, making it easy to arrange meetups without dealing with shipping hassles.

For smaller, branded, or collectible items, Mercari is a solid option. This platform appeals to buyers across the country, and well-known brands like Apple, Nike, Nintendo, and LEGO tend to sell quickly. For instance, a graded Pokémon card might fetch $1,000, a Nintendo DS bundle could go for $111, and LEGO Minifigures might sell for $60. To stay competitive, check Mercari's "See What's Selling" section before you list your items. Categories like electronics, video games, athletic wear, and seasonal decor usually attract plenty of buyers.

When selling online, safety is key. Stick to secure payment methods and avoid options like cryptocurrency, wire transfers, or gift cards. Use the platform’s messaging system to keep a record of conversations, and if something doesn’t feel right, pause and seek advice from someone you trust.

Even small sales can add up quickly. Selling a $60 camera lens or a $50 pair of sneakers here and there could bring in hundreds of dollars within weeks. That extra cash can go straight into your emergency fund, giving you a stronger financial safety net for your travel plans.

8. Use Travel Credit Card Rewards

Travel credit cards can be a lifesaver when unexpected trip expenses pop up, helping you avoid dipping into your emergency fund. Many of these cards come with generous welcome bonuses - typically ranging from 50,000 to 200,000 points - once you meet the initial spending requirements. For instance, as of January 2026, the Amex Platinum card was offering a hefty 175,000-point bonus. Knowing how to make the most of these rewards can lead to immediate savings on travel costs.

You can redeem points for flights, hotel stays, or even as statement credits. On top of that, travel credit cards often include perks like waived fees and built-in protections such as trip cancellation insurance, lost luggage coverage, and rental car collision waivers. Some cards go further by waiving checked bag fees - saving $60 to $70 per person on a round-trip flight - and reimbursing application fees for TSA PreCheck ($78) or Global Entry ($120). Plus, many cards provide access to airport lounges, where you can enjoy complimentary amenities while waiting out travel delays.

That said, it’s important to see rewards as a helpful supplement rather than a replacement for cash savings. Points generally can’t be used for non-travel emergencies, like medical bills or car repairs. And be mindful of the high interest rates that often come with these cards - some charge variable APRs as high as 29.99%. To avoid costly interest, only charge emergency expenses if you’re confident you can pay off the balance in full by the due date.

"As long as you're sure you can pay them off before the bill comes due, your credit limit can act as one form of an emergency fund." - Ethan Steinberg, The Points Guy

9. Try No-Spend Weeks

A no-spend week is a short-term challenge where you stick to spending only on essentials like rent, utilities, and groceries, cutting out anything non-essential. It’s a great way to spot unnecessary expenses and funnel the extra savings straight into your travel emergency fund.

Take BuzzFeed's Hannah Marder, for example. In January 2024, she saved $1,600 by limiting her spending to the bare essentials - groceries, toiletries, and utilities. She avoided restaurants, bars, and impulse purchases on Amazon. To stretch her budget further, she used the "TooGoodToGo" app for discounted food, the Libby app for free library books, and relied on "Buy Nothing" Facebook groups for household items. This method not only saved her money but also reinforced financial discipline, making it a fantastic addition to other savings strategies.

To get started, set clear rules ahead of time. Define what’s truly essential - like housing, utilities, and basic toiletries - and what falls under discretionary spending, such as dining out, coffee runs, new clothes, or online shopping. Delete shopping and food delivery apps from your phone, and make use of what you already have in your pantry.

"There's one simple rule: BUY ONLY WHAT YOU TRULY NEED" - Life with Less Mess

Here’s a pro tip: every time you skip a non-essential purchase, transfer that money immediately into your travel emergency fund. If you feel tempted, jot down the amount and review it later. This not only helps you save quickly but also rewires your habits, breaking the cycle of impulsive spending that can drain your budget.

10. Keep Emergency Funds Separate

Setting up a dedicated savings account specifically for travel emergencies is a practical way to protect your finances. When emergency cash is mixed with your regular checking account, it’s all too easy to dip into it for non-urgent expenses - like a fancy dinner, a flight upgrade, or the latest tech gadget.

By keeping this fund out of sight, you reduce the temptation to spend it. Financial expert Ethan Steinberg suggests storing your emergency fund at a separate financial institution for added discipline:

"One way I try to keep myself in check is by keeping my emergency fund with a different financial institution than my main bank. This way I don't see it every time I log on and I'm not tempted to spend it on frivolous purchases."

Consider opening a high-yield savings account at a different bank. These accounts not only keep your emergency fund separate but also offer competitive annual percentage yields (APYs) - ranging between 3.50% and 5.00% as of late 2025 - so your savings can grow while staying accessible.

The need for emergency funds is clear: only 44% of Americans have enough savings to cover three or more months of expenses, while 25% have no emergency fund at all. Matt Stephens, a Certified Financial Planner at AdvicePoint LLC, underscores the importance of this safety net:

"Emergency funds are important because it keeps people from running up credit card debt or pulling money out of retirement accounts to pay for things, both of which can be devastating to your finances".

To make saving effortless, set up automated transfers from each paycheck into this separate account. Avoid linking a debit card to the account, and use a "wait a month" rule for non-urgent expenses. These small steps can safeguard your emergency fund, ensuring it’s there when you truly need it. This strategy not only secures your financial stability but also strengthens your travel safety net.

Comparison Table

For travelers flying out of Dallas, Joe's Flights offers two alert plans to help you save on airfare and grow your emergency fund.

The Free Plan delivers one flight deal per week via email, including key details like route, price, dates, airline, and a booking link. On the other hand, the Premium Plan - priced at $59 per year - provides unlimited, instant alerts whenever airlines drop prices. This allows you to snag the best fares during the ideal 3-to-7-month booking window, with potential savings of over 80%. For example, a $407 ticket could drop to just $79, leaving you with extra cash to pad your emergency fund.

Here’s a quick breakdown of what each plan offers:

| Feature | Free Plan | Premium Plan |

|---|---|---|

| Price | Free | $59/year |

| Flight Deals | 1 per week | Unlimited, sent immediately |

| Airport Coverage | DFW & Love Field | DFW & Love Field |

| Deal Types | Domestic & international | Domestic & international |

| Booking Details | Route, price, dates, airline, booking link | Route, price, dates, airline, booking link |

For frequent flyers, the savings from just one or two discounted fares can easily cover the cost of the Premium Plan. The extra money can go toward essential expenses like a last-minute flight home, hotel stays, or even medical bills during emergencies.

Conclusion

By blending automation tools, spending adjustments, round-up apps, and flight alerts, you can gradually build a reliable travel emergency fund. Even small, regular contributions can add up over time. For instance, saving $125 every two weeks adds up to $3,000 in a year, providing a solid financial buffer for unexpected situations like medical bills, urgent flights home, or emergency repairs.

"Building a savings of any size is easier when you're able to consistently put money away. It's one of the fastest ways to see it grow." – Consumer Financial Protection Bureau

Treat your emergency fund like a non-negotiable monthly expense, similar to rent or utilities. Automate transfers on payday, stash the money in a high-yield savings account, and avoid using it for anything other than true emergencies. If you do need to dip into it, make replenishing the fund a top priority with your next paycheck.

Even modest savings can significantly improve your financial security. With nearly half of Americans unable to cover a $400 emergency without borrowing or using credit, having any emergency fund puts you in a stronger position. Start small - whether it's $10 a week or a portion of your tax refund - and consistently grow your safety net. These simple strategies ensure you're prepared for unexpected travel expenses without derailing your finances.

FAQs

What are some practical ways to save for travel emergencies on a tight budget?

Saving for travel emergencies, even on a tight budget, is possible with a few simple, consistent habits. Start by setting a clear goal - say $500 or $1,000 - and break it into smaller, more manageable chunks, like $25 a week. To make saving effortless, set up automatic transfers to a dedicated savings account right after each payday.

Look for ways to cut back on non-essential spending. Skipping those daily coffee runs or canceling unused subscriptions can free up extra cash to grow your fund. Got a tax refund or extra income from a side hustle? Try putting at least half of it into your emergency savings. Tools like Joe’s Flights can also help you snag cheap flight deals, letting you keep more of your fund intact for unexpected travel situations.

Keep an eye on your progress and adjust your savings plan as needed. Even small changes, like adding an extra $5 to your weekly savings, can add up over time. By sticking to these steps, you’ll gradually build a travel emergency fund without putting unnecessary pressure on your budget.

How can round-up savings apps help you build a travel emergency fund?

Round-up savings apps offer an effortless way to grow your travel emergency fund. These apps work by rounding up your everyday purchases to the nearest dollar and automatically saving the spare change. For instance, if you buy a coffee for $4.50, the app rounds it up to $5.00 and tucks away the extra $0.50 into a savings account.

Over time, these small contributions can grow into a useful fund without requiring much thought or effort. It's a practical choice for travelers looking to build an emergency stash while sticking to their trip budget.

What’s the best way to use credit card rewards without going into debt?

To get the best out of credit card rewards while steering clear of debt, make it a habit to pay off your balance in full every month. Stick to using a travel rewards card for everyday expenses like groceries or utility bills - things you’d buy regardless - to keep your spending in check.

Look for cards that offer generous sign-up bonuses, set up automatic payments to avoid missing due dates, and keep an eye on your spending. Be sure to redeem your points for flights, hotel stays, or other travel perks before they expire to make the most of your rewards.

Related Blog Posts

Written by Joe's Flights. Spotted something cheaper? Tell us.